Selected Individual and Estate Planning Provisions of the Tax Bills of the House Ways & Means Committee and the Senate Finance Committee

Article

Gibbons Corporate & Finance News - Legislative Tax Alert

November 10, 2017

Obviously, tax reform is front and center in Washington:

-

- The release of the U.S. House Ways and Means Committee tax reform bill on November 2nd initiated the process.

-

- The Ways & Means Committee markup of the bill was completed on November 9.

-

- The Senate Finance Committee released a detailed outline of a tax bill on November 9, which will similarly proceed to Committee markup.

- The final step is the Joint House and Senate Conference to produce a reconciliation bill for submission to the President, projected to occur before the end of this year.

This article summarizes some of the key individual and estate planning provisions of the tax bills just issued by the Ways & Means and Senate Finance Committees. We first provide a chart with respect to some of the more critical individual and estate planning provisions, which briefly compares current law with the draft bills. To see further discussion of items of interest in the chart, please view the text that follows.

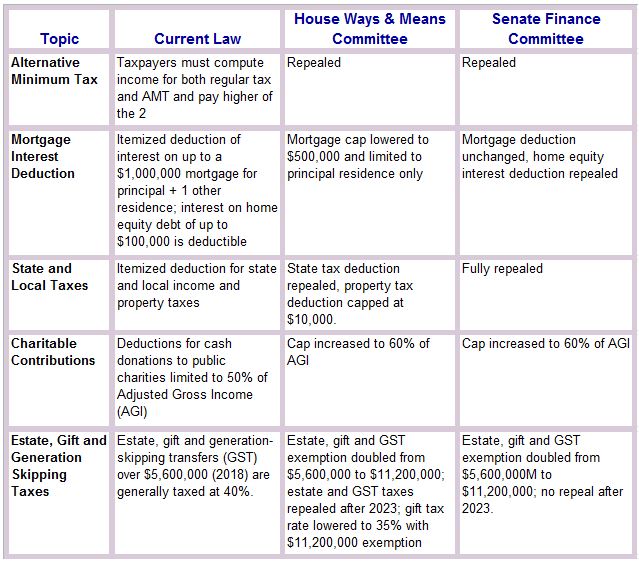

Alternative Minimum Tax

Currently, an alternative minimum tax (“AMT”) is imposed on an individual, estate, or trust in an amount by which the tentative minimum tax exceeds the regular income tax for the taxable year.

House Ways & Means and Senate Finance Committees: Both bills fully repeal the AMT, both individual and corporate.

Mortgage Interest Deduction

Currently, qualified residence interest (interest paid or accrued during the taxable year on both acquisition indebtedness and home equity indebtedness) is deductible on mortgages of up to $1,000,000 and home equity loans up to $100,000. A qualified residence means the taxpayer’s principal residence and one other residence of the taxpayer selected to be a qualified residence.

House Ways & Means Committee: The Ways & Means bill would lower the value of the mortgage upon which interest can be deducted to $500,000 and limit this to the taxpayer’s principal residence, which must have been occupied as such for 5 of the past 8 years.

Senate Finance Committee: The Senate Finance bill leaves the mortgage interest deduction intact but fully repeals the home equity indebtedness deduction.

State and Local Taxes

Currently, individuals are allowed an itemized deduction for the full amount of their state and local income taxes, and for local property taxes as well.

House Ways & Means Committee: The Ways & Means bill would eliminate the deduction for state and local income taxes, and limit the deductibility of property taxes to $10,000. The impact of this would be somewhat mitigated by a doubling of the standard deduction to $24,000, the lowering of tax rates and the elimination of the AMT.

Senate Finance Committee: The Senate Finance bill fully repeals the state and local income and property deductions, and similarly doubles the standard deduction.

Charitable Contributions

Currently, the Internal Revenue Code allows individual taxpayers to reduce their income tax liability by deducting contributions to charities and certain other organizations. For cash donations to public charities and some foundations this is limited to 50 percent of adjusted gross income, subject to certain adjustments. Other donations are further limited in their deductibility.

House Ways & Means and Senate Finance Committees: Both bills will increase the income-based percentage limit for certain charitable contributions by an individual taxpayer of cash to public charities and certain other organizations from 50 percent to 60 percent.

Estate, Gift, and Generation Skipping Taxes

Currently, there is an exemption for estate transfers at death, gifts made during life, and generation skipping tax (“GST”) transfers of $5,490,000. This exemption increases to $5,600,000 as of January 1, 2018. For spouses, any portion of a decedent spouse’s estate exemption not fully utilized during the decedent’s life or at death passes to the surviving spouse (the concept of “portability”). Current law provides for a full step-up of assets owned by a decedent to fair market value at death (“stepped-up tax basis”).

House Ways & Means Committee: The Ways & Means bill would immediately raise the estate, gift, and GST exemption to $11,200,000 (indexed for inflation), and estate and GST taxes would be repealed after 2023. While the Ways & Means bill continues the gift tax after 2023, the tax rate is lowered to 35% with a gift exemption of $11,200,000 (indexed for inflation).

Senate Finance Committee: The Senate Finance bill also immediately doubles the estate, gift, and GST exemption to $11,200,000, but there is no repeal after 2023.

Under both bills, portability between spouses and stepped-up tax basis remain in place. Both proposals represent a dramatic change for wealth transfer planning allowing individuals with large estates to consider making significant lifetime gifts. Further, it is likely existing estate plans will need to be reviewed to account for these changes and the uncertainty whether estate and GST tax repeal would ultimately occur.