Selected Business Provisions of the Tax Cuts and Jobs Act Bills of the House and Senate Finance Committees

Article

Gibbons Corporate & Finance News - Legislative Tax Alert

November 17, 2017

Suddenly, U.S. tax reform has developed momentum, with the House passing its tax proposal on Thursday, November 9 and the Senate Finance Committee adopting its version of a bill late on November 16. This article summarizes some of the key business provisions of these two tax bills.

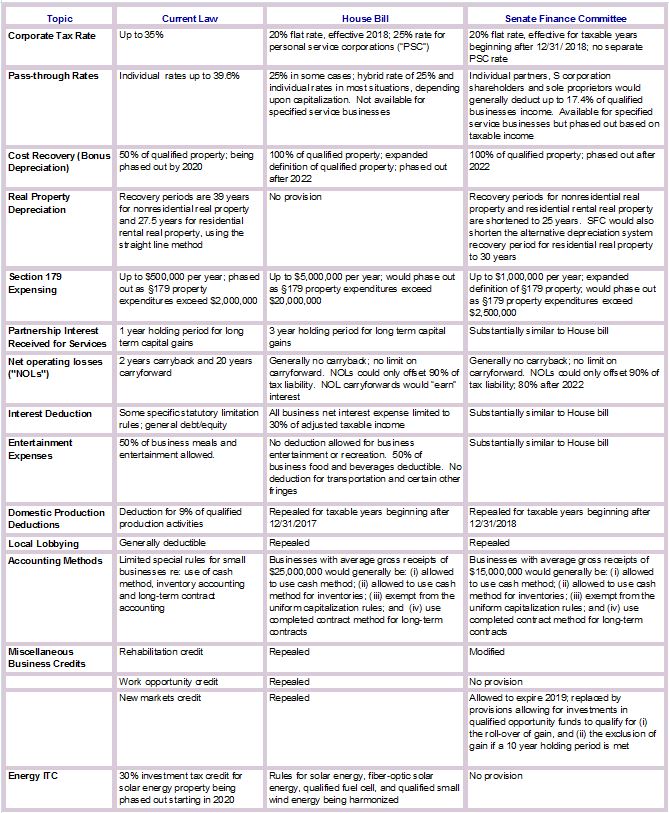

Corporate Tax Rate:

Currently, corporations are subject to tax rates that range up to 35%. Corporations do not benefit from lower long-term capital gain rates.

House: The House bill would lower the corporate income tax rate to a flat 20%, effective for taxable years beginning after 2017. Personal services corporations would be subject to a flat 25% tax rate.

Senate Finance Committee: The SFC bill also provides for a flat 20% rate, but this would not be effective until 2019. No separate rate for personal service corporations.

Pass-through Rates:

Currently, the tax rates that apply to pass-through income, e.g., income allocated by partnerships or S corporations to their partners or shareholders, respectively, are the marginal rates that apply to such partners or shareholders as individuals.

House: Under the House bill, a portion, generally 30%, of net active business activity income would be taxable to the ultimate pass-through individual owner at a 25% rate. If a business is more capital intensive, it can elect into an alternative calculation that might allow a greater portion of the income to be taxed at the 25% rate. The remaining income, e.g., 70%, would be taxable at the ordinary income rates and subject to self-employment taxes, as is often currently the case for the distributive share of partnership income. A lower 9% tax rate would be available for the first $75,000 of net active business taxable income, subject to overall income thresholds. Most service businesses would not be allowed to use the 25% rate, unless they are capital intensive. 100% of passive activity income, as defined under the Section 469 regulations (often real estate rental income or limited partners), would be taxable at the 25% rate. Service business income, limited partners, and rental income generally would be subject to self-employment tax.

Senate Finance Committee: The SFC bill would allow individual partners, S corporation shareholders and sole proprietors to deduct 17.4% of qualified business income, subject to an add-back of 50% of wage-type income. This deduction would be available for specified service businesses but would be phased out as taxable income reached certain specified amounts.

Increased Cost Recovery (Bonus Depreciation):

Currently, taxpayers can write off 50% of the cost of “qualified property” (generally, tangible personal property with a recovery period of 20 years or less). This ratio drops to 40% in 2018, 30% in 2019, and phases out after that.

House: The House bill would allow 100% expensing of the cost of qualified property placed in service after September 27, 2017 and before 2023. Qualified property would include used property acquired by a taxpayer, as long as the taxpayer did not previously use the equipment.

Senate Finance Committee: The SFC bill would also allow 100% expensing of the cost of qualified property placed in service after September 27, 2017 and before 2023. No change in the definition of qualified property.

Section 179 Expensing:

Under current law, businesses can expense up to $500,000 of the cost of Section 179 property (generally limited to depreciable tangible personal property purchased for use in the active conduct of a trade or business) in 2017. The $500,000 limitation is reduced dollar-for-dollar as the total Section 179 property placed in service by a taxpayer exceeds $2,000,000.

House: The House bill would allow businesses to expense up to $5,000,000 of Section 179 property in any one year, for property placed in service after 2017, through 2022. The $5,000,000 amount would phase out as the amount of Section 179 property placed in service exceeded $20,000,000.

Senate Finance Committee: The SFC bill would allow businesses to expense up to $1,000,000 of Section 179 property in any one year, for taxable years after 2017. The $1,000,000 amount would phase out as the amount of Section 179 property placed in service exceeded $2,500,000.

Net Operating Losses:

House: Besides generally eliminating NOL carrybacks, after 2017, the House bill would limit the use of an NOL to 90% of current taxable income, similar to current AMT provisions. Of some interest, the bill would allow NOLs arising after 2017 to be increased by a relatively generous interest factor (4% plus the federal short-term rate).

Senate Finance Committee: The SFC bill would also limit NOLs to 90% of taxable income (80% after 2022), and would generally prohibit carrybacks. NOLs could be carried forward indefinitely.

Interest Deduction Limitations:

House: The House bill would amend Code Section 163(j) to limit net interest deductions for all businesses to 30% of their adjusted taxable income, basically EBITDA. Disallowed amounts of interest expense would carry over for up to five years. Small businesses (average gross receipts of $25,000,000 or less), and real property trades or businesses would be exempt. The House bill would also repeal current Code Section 163(j), which limits the deduction of interest paid or accrued to a non-taxable related party (e.g., a foreign parent) when (i) the payor’s debt-to-equity ratio exceeds 1.5 to 1, and (ii) the payor’s net interest expense exceeds 50% of its adjusted taxable income.

Senate Finance Committee: The SFC bill would also limit net interest deductions for all businesses to 30% of their adjusted taxable income. Disallowed interest would carry over indefinitely. The limitation would not apply to (i) businesses that meet a $15,000,000 gross receipts test, or (ii) real property development, rental, management, leasing or brokerage businesses that elect out. Real property trades or businesses that elect out would be required to use the alternative depreciation system (ADS) to depreciate their nonresidential real property, residential rental property, and qualified improvement property.

Entertainment Expenses:

Currently, businesses can deduct up to 50% of expenses paid or incurred for meals and entertainment directly related to the active conduct of the business.

House: The House bill disallows deductions for business entertainment, amusement or recreation except for 50% of food and beverage expenses and qualifying business meals. In addition, no deduction would be allowed for transportation fringe benefits, benefits related to on-premises gyms or athletic facilities, and certain personal-type amenities, except to the extent that such benefits are treated as taxable to the employee or other person.

Senate Finance Committee: The SFC bill would also disallow deductions for business entertainment, amusement or recreation except for 50% of business food and beverage expenses.

Conclusion:

This alert only addresses some of the more substantial tax items covered by the proposals now under debate in Congress. If you have questions or concerns with how any of these provisions will impact your business, do not hesitate to contact us.

Additional Gibbons Alerts Regarding Tax Reform